When You Want More of a Good Thing: A Leveraged Take on Daily Income

How the T-Squared Lift Series Applies 1.3× Exposure to a Daily 0DTE Covered Call Strategy on SPY

There is a certain kind of investor who looks at a well-designed income strategy and asks: what if I want more of it? Not a different strategy. Not a different exposure. The same mechanism, running a little hotter. The potential for more premium collected and more participation in the underlying. More of the thing that is already working—with clear understanding that “more” cuts both ways.

This is the design brief behind the TappAlpha T-Squared Lift Series. The flagship on the S&P 500 side is the TSPY LIFT ETF (TSYX), which seeks daily investment results, before fees and expenses, of 130% of the daily performance of the TappAlpha SPY Growth & Daily Income ETF (TSPY). [1] The underlying strategy is the same one running inside TSPY: hold SPY, write out of-the-money 0DTE calls1 every trading day, distribute the premium. The Lift overlay applies roughly 30% more exposure to that strategy on a daily basis. It is leverage in the classical sense, and it deserves to be understood as such.

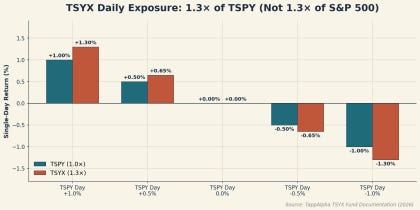

Figure 1: TSYX targets 1.3× of TSPY’s daily performance, not 1.3× of the S&P 500 directly The Income Market That Keeps Growing

The demand for income in 2026 has not been subtle. With the S&P 500’s dividend yield sitting near 1.1%—one of the lowest readings since the late 1990s—and the index at a record 7,126 on April 17, 2026, investors in the distribution phase are in a bind. [2] Ten-year Treasury yields hover near 4.13% and the Federal Funds rate stands at 3.50–3.75%, but shifting allocation to bonds means giving up equity participation. [3] Something has had to give, and the something that gave was the structure of how investors pursue yield.

Derivative income ETFs were the top flow-gaining category within active ETFs in 2025, according to Goldman Sachs Asset Management. [4] Zero-days-to-expiration options have become the baseline of how the S&P 500 options market functions: SPX 0DTE contracts averaged 2.3 million per day in 2025 and represented 59% of total SPX options volume, up from roughly 5% in 2016. [5] The ecosystem is mature. The question for investors already comfortable with a daily covered call approach is whether the base version captures enough of the opportunity—or whether a measured amount of leverage applied to the same mechanism fits the portfolio problem more tightly.

What TSYX Actually Does

TSYX is a leveraged wrapper on TSPY, not a separate strategy with its own logic. [6] TSPY holds SPY—the largest and most liquid S&P 500 ETF in the world—and writes out-of-the-money call options against it every trading day, with each option expiring at the close of that same session. [6] Listed on the Nasdaq since August 14, 2024, TSPY holds three positions: SPY, cash, and the

daily options book. [7]

TSYX, listed on the Nasdaq and launched January 7, 2026, seeks daily investment results of 130% of TSPY’s daily performance. [1] The SPY exposure embedded in TSPY becomes roughly 1.3× SPY exposure in TSYX. The premium collected from the daily 0DTE calls becomes roughly 1.3× that premium. And critically, drawdowns in TSPY are magnified by the same factor on a daily basis.

This is not a novel financial instrument. Daily-reset leveraged ETFs have existed for more than two decades. What is relatively new is applying the leveraged-daily-reset chassis to a covered call strategy rather than a pure index exposure. The combination changes the math of what investors are taking on—which is exactly why the mechanics matter more here than in a typical index product.

Why the “Daily” in “Daily Reset” Matters

Anyone considering a leveraged fund needs to understand the single most important feature of how these products work: they reset daily. TSYX does not seek to deliver 130% of TSPY’s performance over a week, month, or year. It seeks 130% on each trading day, independently. [1]

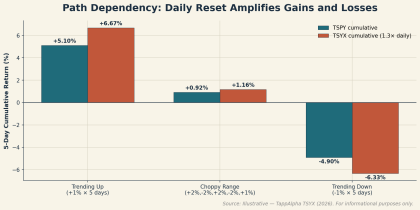

Figure 2: Path dependency — daily reset can amplify gains in trends and drag in chop

Over multi-day periods, the compounding of daily 1.3× returns can produce outcomes that diverge—sometimes meaningfully—from a simple “1.3× the holding period return” calculation. In trending markets, daily compounding can work in the investor’s favor, potentially producing multi-day returns greater than 1.3× the underlying’s move. In choppy, sideways markets, the same compounding can produce “volatility drag,” where realized returns lag a 1.3× calculation. This is disclosed in every leveraged ETF prospectus in the industry and is the mechanical consequence of the design.

For income investors considering TSYX, the implication is specific. An allocation should be thought of as a tactical tool for expressing conviction on the underlying TSPY strategy over relatively defined periods—not as a “set it and forget it” decade-long holding.

When the Market Favors This Structure

The current market has characteristics a measured-leverage income strategy is specifically designed to navigate.

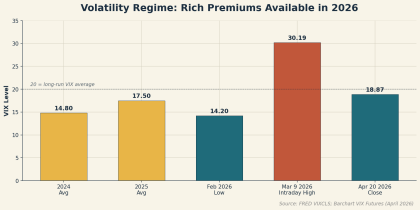

Figure 3: VIX regime 2024–2026 — richer premiums available on the other side of March’s spike

The Cboe Volatility Index, or VIX, closed at 18.87 on April 20, 2026, off its March intraday high above 30 but still elevated relative to the 12–14 readings that dominated 2024. [8] Higher implied volatility means richer option premiums, and a 1.3× exposure to a premium-collection strategy captures more of that opportunity per dollar invested. The earnings backdrop supports the underlying index: S&P 500 Q1 2026 earnings growth is running at 13.2% blended, the sixth consecutive quarter of double-digit growth. [9] And the rotation dynamic—the S&P 500 fell 4.98% in March then rallied 13 consecutive sessions to a new high—rewards strategies that collect premium every day rather than on monthly expirations. [2]

The Risks That Deserve Top Billing

Leverage is the defining feature of TSYX, and the risks should be stated clearly.

Drawdown magnification. If TSPY declines 10% on a given day, TSYX is designed to decline roughly 13% on that same day. Over multi-day periods with continued declines, the daily compounding of 1.3× losses can produce outcomes meaningfully worse than 1.3× the peak-to trough drawdown of TSPY. The premium collected partially offsets drawdowns—but “partially” is the operative word.

Upside cap. The daily covered call strategy limits participation in sharp single-day rallies in SPY. A leveraged wrapper on a capped strategy does not remove that cap—it just runs more of the capped exposure. In relentless one-direction bull markets, an unleveraged SPY position will generally outperform TSYX.

Path dependency. As discussed, the daily reset means multi-day returns are not simply 1.3× the underlying’s multi-day return. This is true of every daily-reset leveraged ETF.

Short operating history. TSYX launched on January 7, 2026. [1] Investors should review the prospectus for the full risk disclosures, including those specific to new funds, options strategies, and leveraged products.

Where TSYX Might Fit in a Portfolio

TSYX is a tactical allocation, not a core holding. For investors who have already decided a daily 0DTE covered call strategy on SPY fits their income needs, TSYX offers a way to express that conviction with a measured amount of leverage—1.3× rather than the 2× or 3× common elsewhere in the leveraged ETF ecosystem. The “light leverage” framing is intentional. It is meant to provide more of what TSPY delivers, not to convert a measured income strategy into a speculative trade.

A reasonable framing: a larger position in TSPY and a smaller, more tactical position in TSYX— using the leveraged version for periods where volatility is elevated and the premium environment is richer, and trimming it when volatility compresses. The appropriate sizing depends entirely on the individual investor’s circumstances, risk tolerance, and time horizon.

The S&P 500 is at a record high. The options market is printing 2.3 million SPX 0DTE contracts a day. The volatility risk premium is one of the few structural inefficiencies that remains harvestable at scale in 2026. For investors who have conviction in the daily 0DTE covered call approach and want to run it a little hotter—with clear eyes about the mechanics, the path dependency, and the magnified drawdowns—TSYX is a 1.3× daily reset wrapper on the same engine. It is more of a good thing. The discipline is making sure “more” is the right answer for the problem at hand.

Definitions and Disclosure:

1An out-of-the-money (OTM) call option is a call option where the strike price is above the current market price of the underlying asset.

This content is sponsored by TappAlpha. The Lead-Lag Report has been compensated for the publication of this material. The views and opinions expressed herein are those of the author and do not necessarily reflect the views of TappAlpha or its affiliates.

This material is for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy, sell, or hold any securities, including TSYX or TSPY.

The fund currently expects, but does not guarantee, to make distributions on a monthly basis. Distributions may exceed the fund’s income and gains for the taxable year. Distributions in excess of the fund’s current and accumulated earnings and profits will be treated as a return of capital.

Investors should carefully consider the investment objectives, risks, charges and expenses of the ETF. This and other important information about the Fund are contained in the prospectus, which should be read carefully before investing.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Returns less than one year are not annualized.

An investment in the Fund is subject to risks, including the possible loss of the principal amount invested. This Fund may not be suitable for all investors.

The Fund seeks leveraged exposure to the performance of its reference asset and does not invest directly in equity securities in the same manner as a traditional equity fund. Exchange-Traded Funds (ETFs) trade like stocks, are subject to investment risk, and will fluctuate in market value. Transactions in shares of ETFs will result in brokerage commissions, which will reduce returns. There is no assurance that the Fund’s investment process will consistently lead to successful investing. As of the date of this prospectus, the Fund has no operating history and currently has fewer assets than larger funds. Like other new funds, large inflows and outflows may impact the Fund’s market exposure for limited periods of time. This impact may be positive or negative, depending on the direction of market movement during the period affected.

Short term performance, in particular, is not a good indication of the fund’s future performance, and an investment should not be made based solely on returns. The Fund does not have a track record of reporting to investors or widely available research coverage which may result in price volatility. As of the date of this prospectus, the Fund has a limited operating history and currently has fewer assets than larger funds.

Leverage Risk. The Fund seeks daily investment results, before fees and expenses, of 130% of the daily performance of TSPY. The Fund’s use of leverage to seek its daily investment objective will magnify gains and losses. As a result, the Fund is riskier than alternative investments that

do not use leverage and should not be used by investors who do not understand the risks of leveraged investment products.

Daily Reset Risk / Compounding Risk. The Fund does not seek to achieve its stated investment objective for a period of time different than a trading day. The daily rebalancing of the Fund’s exposure, combined with the compounding of daily returns over time, means the Fund’s performance over periods longer than a single trading day can differ significantly— potentially substantially—from 130% of the performance of TSPY over that same period. This divergence is more pronounced in volatile markets and over longer holding periods.

Options Contract Risk. The Fund invests in options contracts that are based on the value of an index. This subjects the Fund to certain of the same risks as if it owned shares of companies that comprised the index, even though it does not own shares of companies in the index. The Fund will have exposure to declines in the underlying index.

0DTE Options Risk. Due to the short time until their expiration, 0DTE options are more sensitive to sudden price movements and market volatility than options with more time until expiration. 0DTE options may also suffer from low liquidity. The bid-ask spreads on 0DTE options can be wider than with traditional options, increasing the Fund’s transaction costs and negatively affecting its returns.

Distributor: Foreside Fund Services, LLC, Member FINRA.

Footnotes

1. TappAlpha, TSYX (TSPY LIFT ETF) fund page, April 2026.

2. Seeking Alpha, “S&P 500 Clocks New Record High As Near-Record Winning Streak Continues,” April 20, 2026; Clark Capital Management Group, March 2026 Benchmark Review; Multpl, S&P 500 Dividend Yield by Month, April 2026.

3. Federal Reserve Economic Data (FRED), 10-Year Treasury Constant Maturity Rate and Federal Funds Effective Rate, April 2026.

4. Goldman Sachs Asset Management, “Why 2026 will be another big year for derivative income & defined outcome ETFs,” February 2026.

5. Cboe Global Markets, “The State of the Options Industry: 2025.”

6. TappAlpha, TSPY Fund Prospectus, April 30, 2025.

7. TappAlpha, TSPY fund page, April 2026; Stock Analysis, TSPY ETF data, April 2026.

8. Federal Reserve Bank of St. Louis (FRED), CBOE Volatility Index, April 20, 2026; Barchart S&P 500 VIX March 2026 futures data.

9. FactSet, “S&P 500 Earnings Season Update,” April 17, 2026.

DISCLAIMER – PLEASE READ: This is a sponsored article for which Lead-Lag Publishing, LLC has been paid a fee. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided in the article or make any representation as to its quality. All statements and expressions provided in this article are the sole opinion of TappAlpha and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided in the discussion. The content in this writing is for informational purposes only. You should not construe any information or other material as investment, financial, tax, or other advice. A participant may have taken or recommended any investment position discussed, but may close such position or alter its recommendation at any time without notice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in any jurisdiction. Please consult your own investment or financial advisor for advice related to all investment decisions.