Why Tactical Allocation Funds Like ATACX Matter in a Late-Cycle Environment

Key Highlights

The U.S. economy is showing multiple late-cycle signals, including slowing growth, a persistent yield-curve inversion, and weakening leading indicators.¹²³

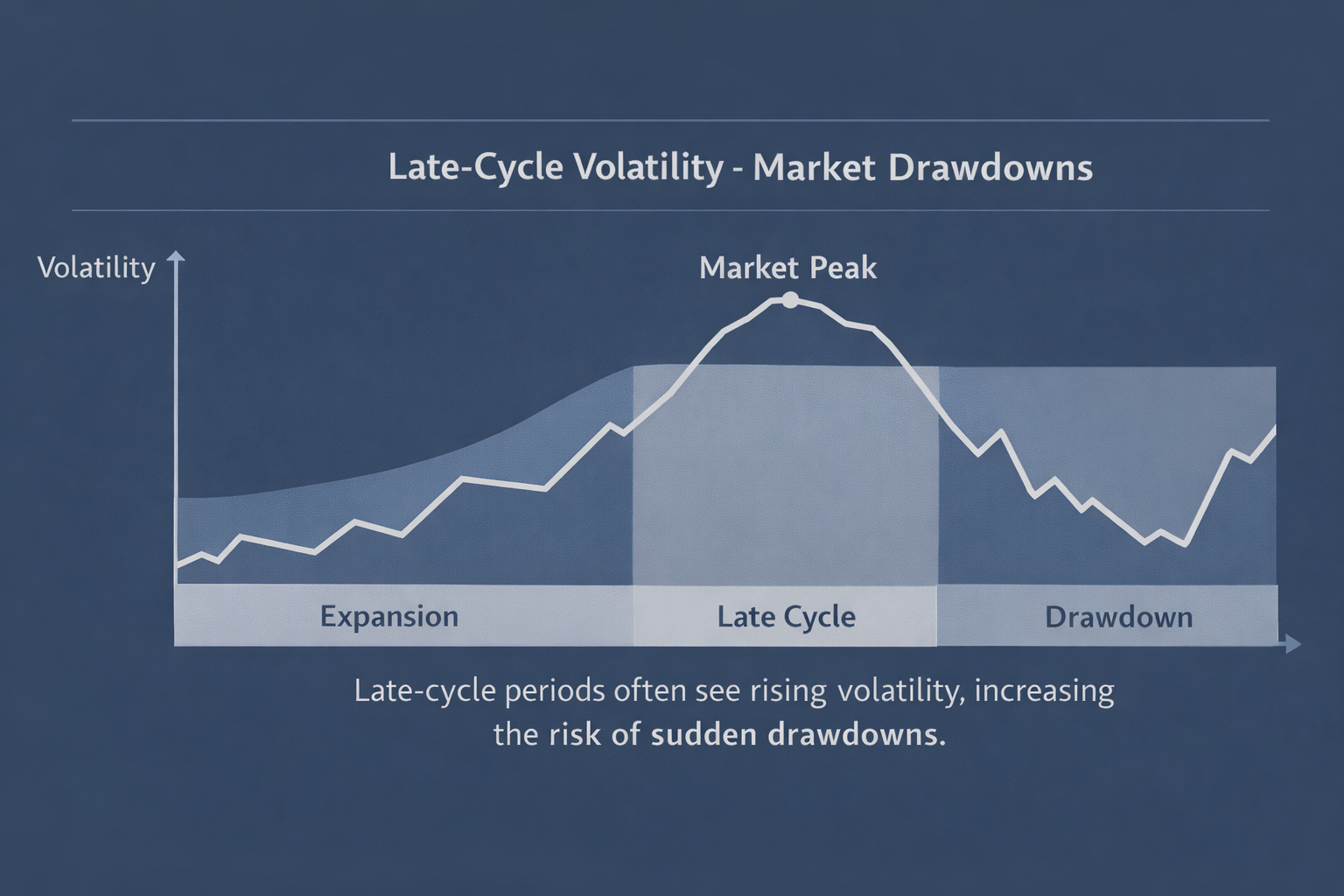

Late-cycle environments increase the risk of sudden market reversals, making static portfolio allocations more vulnerable.

Tactical allocation funds like the ATAC Rotation Fund (Ticker: ATACX) are designed to adapt by rotating between equities and U.S. Treasuries based on objective market signals rather than forecasts.⁶⁷

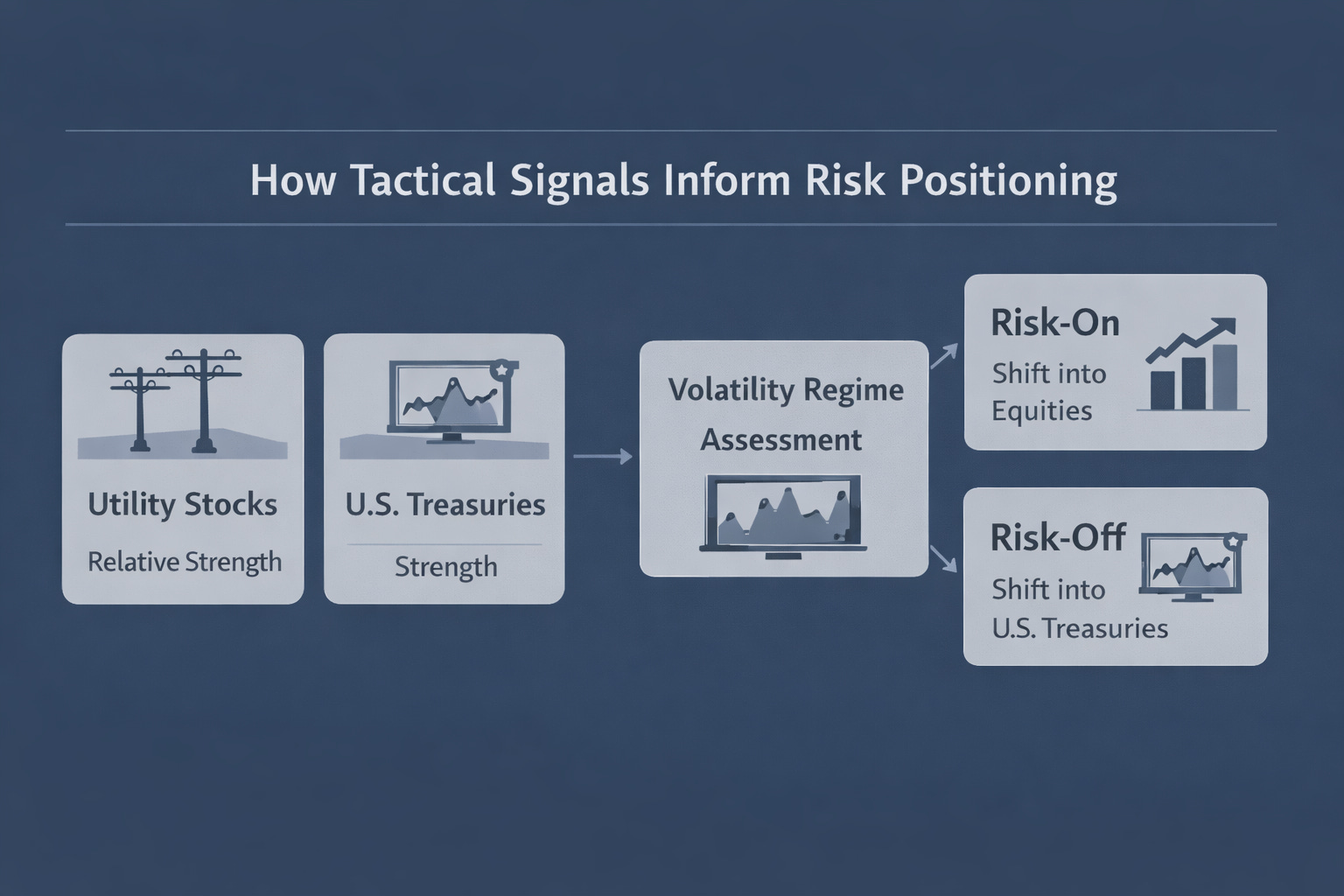

ATACX relies on volatility-sensitive indicators, including relative performance of utilities and Treasuries, to determine when to shift between risk-on and risk-off positioning.

While tactical strategies may lag during extended bull markets, they can offer diversification and risk-management benefits during periods of rising uncertainty.⁸⁹

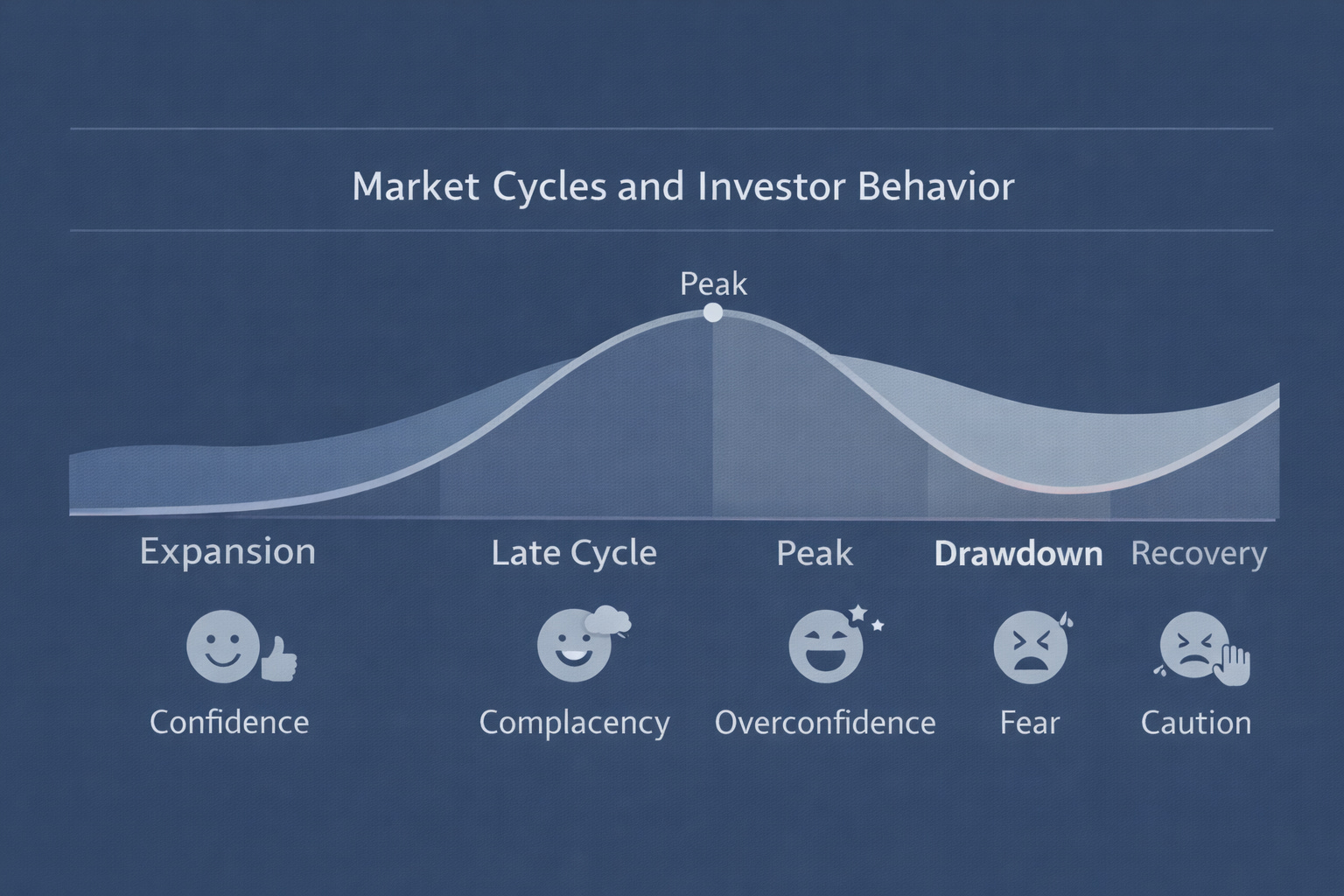

Economic signals increasingly suggest that the current expansion is entering a mature phase. Growth has moderated, interest rates remain restrictive by historical standards, and investors are once again debating whether the next downturn is imminent or still a distance away. Late-cycle environments rarely end with a clear signal. Instead, they are defined by uncertainty, uneven growth, and rising sensitivity to shocks. In that setting, portfolio construction becomes less about maximizing upside and more about managing risk without abandoning opportunity altogether.

This backdrop helps explain renewed interest in tactical allocation strategies, particularly funds designed to dynamically adjust exposure as conditions evolve. The ATAC Rotation Fund (ATACX) is one such approach. Rather than committing to a fixed mix of stocks and bonds, ATACX seeks to rotate between risk assets and defensive assets based on market-derived signals. The objective is not prediction, but adaptation. In a late-cycle economy where turning points are difficult to time, that distinction matters.

Slowing Growth and Late-Cycle Signals

By traditional measures, U.S. economic momentum has softened. After a relatively strong post-pandemic expansion, growth expectations have drifted lower as higher borrowing costs and tighter financial conditions work through the economy. Gross domestic product growth moderated through 2025, with forward-looking indicators pointing toward further deceleration into 2026.¹ While quarterly data have been uneven, the broader trend suggests diminishing resilience rather than acceleration.

The Conference Board’s Leading Economic Index reinforces that view. The index declined steadily through much of 2025, a pattern that historically has preceded periods of economic slowdown.² Although the timing of recessions varies, persistent weakness in leading indicators has often signaled that risks are skewed to the downside rather than the upside.

Bond markets have been even more explicit. The U.S. Treasury yield curve has remained inverted for an extended period, with short-term yields exceeding long-term yields. Historically, prolonged inversions have preceded economic contractions with notable consistency.³ While the economy has so far avoided a formal recession, the persistence of this signal suggests underlying fragility.

Labor market conditions also reflect late-cycle dynamics. Job growth has cooled from post-pandemic highs, and the unemployment rate has drifted upward from cycle lows.⁴ These shifts do not indicate crisis, but they do point to a labor market that is no longer tightening and may be less capable of absorbing shocks.

At the same time, monetary policy has begun to pivot. After raising rates aggressively to contain inflation, the Federal Reserve has signaled a willingness to ease as growth risks rise.⁵ Historically, such transitions tend to occur closer to the end of economic cycles than the beginning.

Taken together, these factors describe an expansion that is aging rather than accelerating. For investors, the challenge is not simply identifying risk, but responding to it without relying on binary decisions such as exiting the market entirely.

How ATACX Approaches Late-Cycle Risk

The ATAC Rotation Fund is structured around that challenge. Instead of maintaining constant exposure to equities, the fund rotates between stock and Treasury bond allocations based on quantitative signals tied to market volatility. The strategy evaluates relative performance trends in areas that have historically acted as early indicators of risk, particularly U.S. Treasury bonds and utility stocks.⁶

Utilities and Treasuries often attract capital during periods of rising uncertainty. When investors become more risk-averse, these assets tend to outperform broader equity markets. ATACX uses these relationships as inputs to determine whether the market environment is more conducive to taking risk or stepping back. When conditions appear favorable, the fund allocates to equity exposure. When signals deteriorate, it shifts defensively into Treasuries.⁷

Portfolio adjustments are triggered by predefined thresholds rather than subjective judgments about economic headlines or market sentiment. That design aims to reduce emotional decision-making, which can be particularly costly during late-cycle periods when volatility tends to rise.

Importantly, the strategy allows for full shifts between risk-on and risk-off positioning. ATACX can move entirely into equity exposure during favorable conditions or fully into Treasury bonds when defensive signals dominate. This flexibility differentiates it from balanced funds that maintain static allocations regardless of changing conditions.

Potential Role in a Portfolio

In practical terms, ATACX seeks to address a common late-cycle dilemma. Investors often want continued participation in market upside, but they also want preservation if conditions deteriorate quickly. Traditional portfolios may struggle to deliver both simultaneously. Tactical allocation strategies attempt to bridge that gap by adjusting exposure dynamically rather than relying on fixed assumptions.

Because ATACX rotates between assets with historically different risk profiles, its return pattern may diverge from that of traditional stock-heavy portfolios. Over time, that can provide diversification benefits, particularly during periods when volatility spikes and correlations shift.⁸ The trade-off is that tactical strategies may lag during extended periods of low volatility and strong equity performance, when defensive positioning proves unnecessary.

That trade-off is central to understanding the strategy. Tactical allocation is not designed to outperform equities during every market environment. It is designed to respond to changing conditions, even when those responses temporarily detract from performance. In late-cycle markets, where reversals can be sudden and severe, that responsiveness can be a meaningful attribute.

Risks and Considerations

As with any active strategy, ATACX is not without risks. Signals can misfire, leading the fund to rotate defensively before a market pullback that never materializes. During prolonged bull markets, such positioning can result in underperformance relative to passive equity benchmarks.⁹

Cost is another consideration. Tactical funds typically carry higher expenses than passive index funds, reflecting the complexity of their strategies and the frequency of portfolio adjustments. Tax efficiency may also be a concern in taxable accounts due to higher turnover.

These factors underscore that ATACX is not a universal solution. It is a specialized tool designed for investors who prioritize risk management and adaptability, particularly in environments where economic and market signals are mixed rather than clear.

Why Tactical Allocation Matters Now

Late-cycle markets rarely offer clean exit points. More often, they produce extended periods of uncertainty punctuated by sharp drawdowns. In that context, the ability to adapt may matter more than the ability to forecast. Tactical allocation funds like ATACX are built around that premise.

Rather than attempting to predict when a recession will arrive, the strategy responds to observable shifts in market behavior. That approach aligns with the reality that markets often turn before economic data confirms a slowdown. For investors seeking a way to remain engaged while acknowledging rising risks, tactical allocation offers an alternative to static positioning.

Whether the next downturn arrives soon or remains delayed, the current environment places a premium on flexibility. ATACX represents one way to pursue that flexibility, rotating between offense and defense as conditions evolve. In a late-cycle economy where certainty is scarce, that adaptability helps explain why tactical allocation funds continue to attract attention.

Consider ATACX. I believe in it. I wouldn’t have launched the fund if I didn’t.

Footnotes

The Conference Board, Global Economic Outlook 2025–2026, December 2025.

The Conference Board, “US Leading Economic Index Declined Again in September,” press release, December 9, 2025.

Wellington Management, “Learning to Love a Late-Cycle Environment,” Wellington Institutional Insights, 2025.

Callum Jones and Aliya Uteuova, “The 2025 US Economy in Charts,” The Guardian, December 28, 2025.

Federal Reserve Board, Monetary Policy Report, November 2025.

Marley Jay, “Falling Lumber Prices Serve as a Stock Market Warning Indicator,” Business Insider, July 20, 2021.

ATAC Funds, ATAC Rotation Fund Prospectus, June 5, 2025.

ATAC Funds, “Overview of ATAC Rotation Strategies,” atacfunds.com, accessed December 29, 2025.

ATAC Funds, “Frequently Asked Questions: ATAC Rotation Fund,” atacfunds.com, accessed December 29, 2025.

The Russell 2000 Index is a stock market index that tracks the performance of 2,000 small-cap US companies, serving as a key benchmark for small-cap stocks and a barometer for the US economy

The Nasdaq 100 is a stock market index comprising the 100 largest non-financial companies listed on the Nasdaq stock exchange, weighted by modified market capitalization

The Standard and Poor’s 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States.

Past performance is no guarantee of future results.

The Fund’s investment objectives, risks, charges, expenses and other information are described in the statutory or summary prospectus, which must be read and considered carefully before investing. You may download the statutory or summary prospectus or obtain a hard copy by calling 855-ATACFUND or visiting www.atacfunds.com. Please read the Prospectuses carefully before you invest.

Fund Risks: An investment in the Fund is subject to numerous risks including the possible loss of principal. There can be no assurance that the Fund will achieve its investment objective. Equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate. As with all ETFs, Fund shares may be bought and sold in the secondary market at market prices. The market price normally should approximate the Fund’s net asset value per share (NAV), but the market price sometimes may be higher or lower than the NAV. There are a limited number of financial institutions authorized to buy and sell shares directly with the Fund, and there may be a limited number of other liquidity providers in the marketplace. There is no assurance that Fund shares will trade at any volume, or at all, on any stock exchange. Low trading activity may result in shares trading at a material discount to NAV. Please see the prospectus and summary prospectus for a complete description of principal risks.

The Fund’s investments will be concentrated in an industry or group of industries to the extent the portfolio manager deems it appropriate to be so concentrated. In such event, the value of Shares may rise and fall more than the value of shares that invest in securities of companies in a broader range of industries.

Investing involves risk including the possible loss of principal.

JOJO is distributed by Foreside Fund Services, LLC.

ATACX is distributed by Quasar Distributors, LLC.