YYY: The Income Illusion or the Ultimate Credit Barometer?

Why a high-yield CEF basket can amplify both income and instability.

Key Highlights

YYY provides exposure to a rules-based basket of high-income closed-end funds through a single ETF wrapper.¹

The strategy introduces layered risks: credit exposure, embedded leverage inside underlying CEFs, and premium/discount dynamics.⁴⁵

Performance is highly sensitive to liquidity conditions, credit spreads, and interest-rate volatility.¹⁷

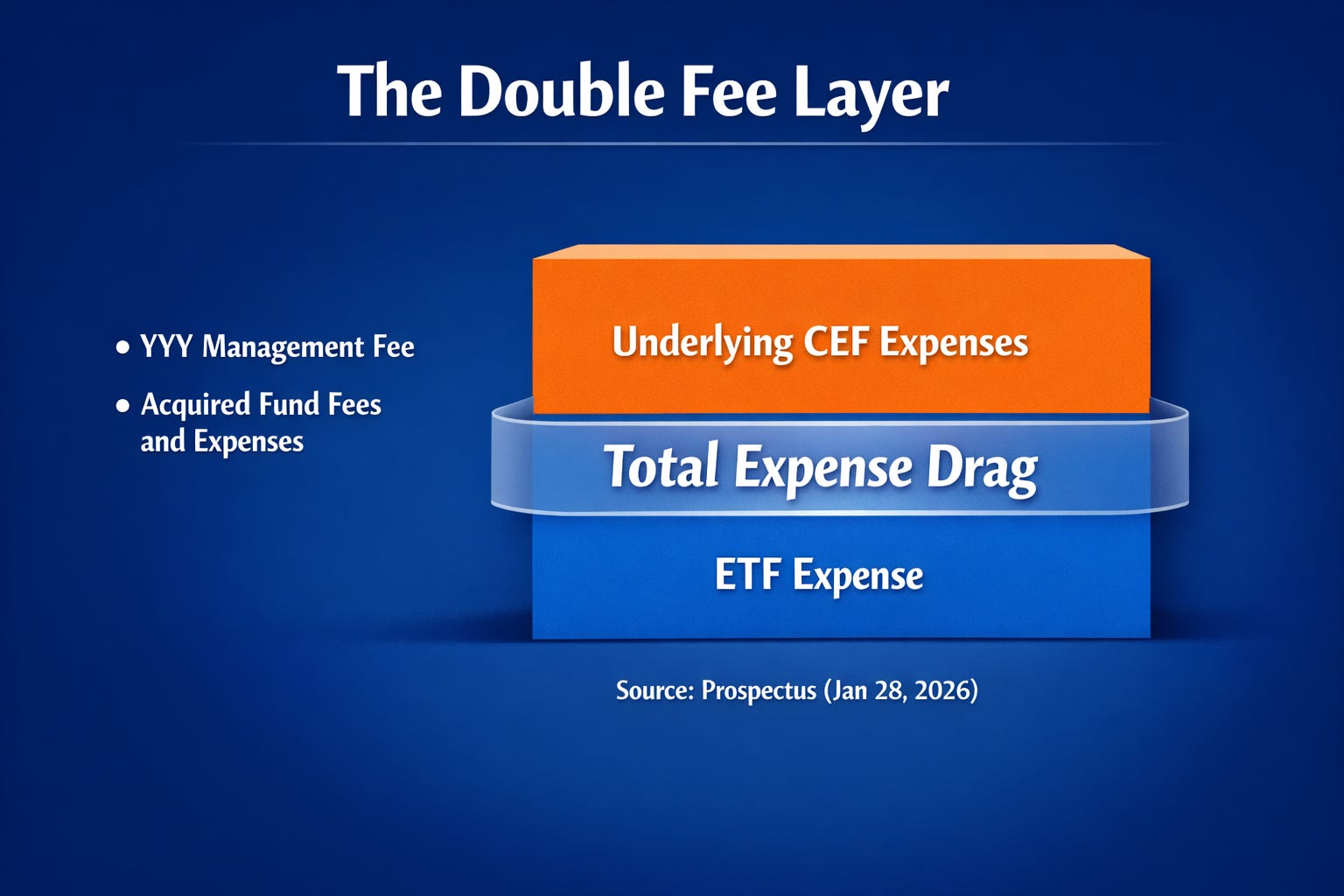

The fund’s two-tier expense structure raises the hurdle rate relative to simpler bond ETFs.⁴

YYY may function best as a tactical income satellite rather than a core bond substitute.⁴

Why YYY Keeps Showing Up Now

Cash worked unusually well for a stretch. After aggressive rate hikes, money markets and short-duration vehicles finally paid investors for patience. That backdrop shifted when the Federal Reserve signaled a slower, more cautious path following earlier easing and a subsequent hold, noting inflation remains somewhat elevated and uncertainty persists.¹

That shift reframes the income discussion. If policy rates move lower over time, short-term instruments may lose some relative appeal. Investors begin searching for the next rung on the income ladder. The more important question becomes what risks are embedded in the income stream being pursued.

YYY packages a segment of the market that many investors rarely access directly: closed-end funds. The idea sounds simple. Buy one ETF, gain diversified exposure to income-oriented CEFs, and receive monthly distributions.

The structure is more complex than the headline. YYY ties results to credit conditions, interest-rate volatility, and investor sentiment toward closed-end funds themselves.²

The thesis can be stated plainly. YYY may function as an income satellite during periods when economic growth remains intact and credit stress stays contained. That same structure can amplify downside when liquidity tightens and discounts widen across the CEF universe. The ETF wrapper simplifies access. It does not remove structural risk.⁴

What YYY Actually Owns

YYY is a fund-of-funds. It does not buy individual bonds in the manner of a traditional corporate bond ETF. Instead, it tracks the Nasdaq CEF High Income Index and invests in shares of up to 60 U.S.-listed closed-end funds selected using rules that emphasize income characteristics, liquidity, and discounts to net asset value.³

That methodology reveals the portfolio’s personality. The screen tilts toward funds that distribute higher income and often trade at discounts. Discounts frequently reflect investor skepticism or structural complexity. In effect, YYY leans into segments the broader market may already view cautiously.³

The underlying CEFs span multiple categories, including taxable credit, municipal bonds, preferred securities, convertibles, REIT exposure, and other income-generating strategies.⁴ Investors are not simply buying high yield bonds. They are buying a rotating mix of managers and mandates, some of which may employ leverage.⁴

Costs deserve attention. YYY charges its own management fee. Shareholders also indirectly bear the operating expenses of the underlying CEFs, reflected as acquired fund fees and expenses.⁴ This layered structure raises the performance hurdle. Market tailwinds must overcome two sets of costs before investors see net results.

Operationally, YYY trades intraday on an exchange like other ETFs. Shares can trade at premiums or discounts to NAV, though the creation and redemption mechanism generally helps keep deviations contained under normal conditions.² The ETF wrapper enhances accessibility. It does not simplify the underlying exposures.

Closed-End Funds: Discounts, Leverage, and Distribution Reality

Understanding YYY requires understanding CEF mechanics.

The U.S. Securities and Exchange Commission describes publicly traded closed-end funds as pooled vehicles whose shares trade on exchanges and whose market prices may sit above or below the value of their underlying holdings.⁵

This premium-or-discount feature introduces a second valuation layer. A traditional bond fund’s NAV moves with bond prices. A CEF’s market price moves with NAV and investor sentiment. Financial Industry Regulatory Authority explains that supply and demand determine share price, while NAV reflects underlying asset values.⁶

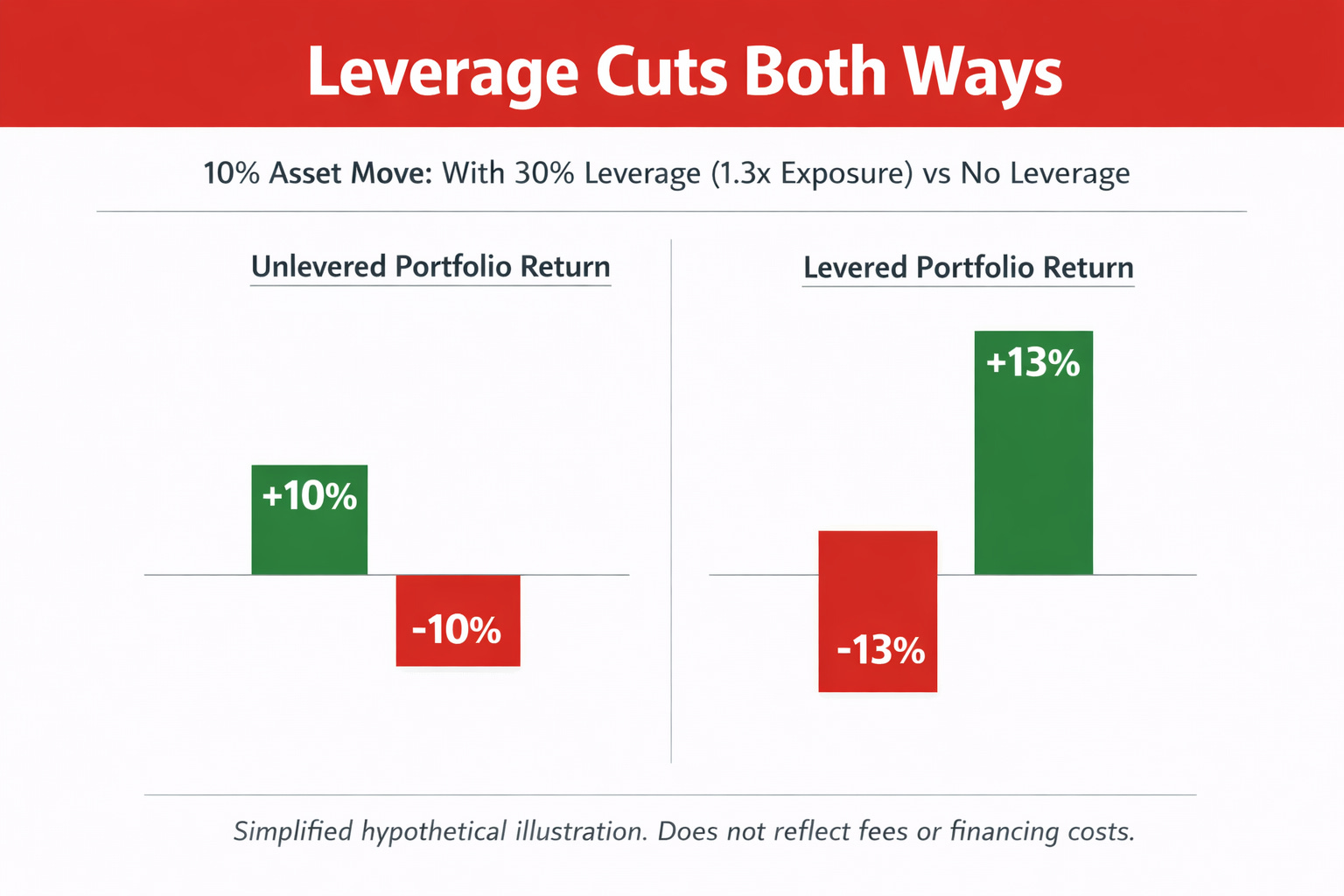

Leverage adds another dimension. Many CEFs employ borrowing or structural leverage to enhance income. The SEC notes that leverage can magnify gains and losses.⁵ In a stable or easing rate environment, leverage may support income. In a rising-rate or tightening liquidity environment, leverage can increase volatility and pressure returns.