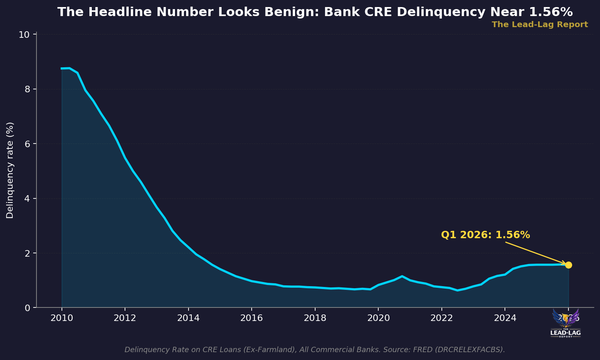

Three Holds, Treasuries Hedge

Three of four signals favor risk-on positioning. The Treasury rotation lone holdout continues to flag a defensive undertone beneath the surface.

Special Announcement

What if you could target only the strongest performers in an index?

Columbia Research Enhanced Core ETF (RECS) leverages our firm’s quantitative research by investing in our highest-rated stocks from the Russell 1000. The result is an ETF with reduced drag and enhanced return potential at an attractive price point.

Potential benefits of RECS:

· Aims to optimize core equity exposure

· Sector-neutral to the Russell 1000

· Competitive expense ratio of 15 basis points1

1 Net and gross expense ratio. The fund’s expense ratio is from the most recent prospectus.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Fund before investing. To obtain a prospectus containing this and other important information, please visit https://www.columbiathreadneedleus.com/etf to view or download a prospectus. Read the prospectus carefully before investing.

Investing involves risks, including the risk of loss of principal. Market risk may affect a single issuer, sector of the economy, industry or the market as a whole. The fund is passively managed and seeks to track the performance of an index. There is no guarantee that the index and, correspondingly, the fund will achieve positive returns. Risk exists that the index provider may not follow its methodology for index construction. Errors may result in a negative fund performance. The fund’s net asset value will generally decline when the market value of its targeted index declines. The fund concentrates its investments in issuers of one or more particular industries to the same extent as the underlying index. Investments in a narrowly focused sector may exhibit higher volatility than investments with a broader focus. Investments selected using quantitative methods may perform differently from the market as a whole and may not enable the fund to achieve its objective. Investment in larger companies may involve certain risks associated with their larger size and may be less able to respond quickly to new competitive challenges than smaller competitors. Investments in mid-cap companies often involve greater risks that investments in larger companies and may have less predictable earning and be less liquid than the securities in larger firms. Growth securities, at times, may not perform as well as value securities or the stock market in general and may be out of favor with investors. Value securities may be unprofitable if the market fails to recognize their intrinsic worth or the portfolio manager misgauged that worth. Although the fund’s shares are listed on an exchange, there can be no assurance that an active, liquid or otherwise orderly trading market for shares will be established or maintained. The Fund may have portfolio turnover, which may cause an adverse cost impact. There may be additional portfolio turnover risk as active market trading of the fund’s shares may cause more frequent creation or redemption activities that could, in certain circumstances, increase the number of portfolio transactions as well as tracking error to the Index and high levels of transactions increase brokerage and other transaction costs and may result in increased taxable capital gains.

ETF shares are bought and sold at market price (not NAV) and are not individually redeemable. Investors buy and sellshares on a secondary market. Shares may trade at a premium or discount to the NAV. Only market makers or “authorized participants” may trade directly with the Fund(s), typically in blocks of 50,000 shares.

Shares are not FDIC insured, may lose value, and have no bank guarantee.

For broker/dealer or institutional use only.

Columbia Management Investment Advisers, LLC serves as the investment manager to the ETFs. The ETFs are distributed by ALPS Distributors, Inc., which is not affiliated with Columbia Management Investment Advisers, LLC, Columbia Management Investment Distributors, Inc. or its parent company Ameriprise Financial, Inc. Columbia Management Investment Distributors, Inc., LLC (Member FINRA | SIPC) is a marketing agent for the ETFs. Columbia Threadneedle Investments is the global brand name of the Columbia and Threadneedle group of companies.

DISCLAIMER – PLEASE READ: This is sponsored advertising content for which Lead-Lag Publishing, LLC has been paid a fee. The information provided in the link is solely the creation of Columbia Threadneedle. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided in the link or make any representation as to its quality. All statements and expressions provided in the link are the sole opinion of Columbia Threadneedle and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided in the link.

Three Holds, Treasuries Hedge

SIGNAL SUMMARY

Key Takeaways:

• Signal 1 (Beta Rotation) remains Risk-On with the XLU/SPY 4-week RoC at -0.82%. The S&P 500 continues to outperform Utilities, signaling that risk appetite still favors broad equity over defensive sectors. The allocation remains 100% SPY.

• Signal 2 (Treasury Rotation) is RISK-OFF on the latest May month-end reading. TLT returned 0.16% in May versus IEF at -0.35%. Long-duration bonds outperformed intermediate maturities, a defensive risk-appetite indicator. The signal will hold this reading through the end of June. The current allocation tilts toward long-duration Treasuries (VLGSX/TLT).

• Signal 3 (Lumber/Gold) is RISK-ON on the latest 13-week relative-performance reading. Lumber’s 13-week return of 1.30% exceeds gold’s -11.72%. All seven sub-strategies are positioned offensively, with cyclical exposures favored over defensive bond pairs.

• The S&P 500 at 7,383.73 sits +7.7% above its 200-day SMA of 6,858.26. Signal 4 remains Risk-On, with the allocation set to SSO (2x leveraged S&P 500). Trend remains intact even after Friday’s broad equity selloff.

MARKET COMMENTARY

The framework reads 3-1 Risk-On this week. Three of the four intermarket indicators favor offensive positioning, with the Treasury Rotation signal the lone defensive holdout on the May month-end reading. The S&P 500 closed at 7,383.73 on June 5 — a sharp single-day selloff capped the week — with the index still sitting +7.7% above its 200-day moving average of 6,858.26. Trend, beta rotation, and lumber/gold remain aligned with risk, but the long-duration Treasury bid suggests pockets of caution beneath the surface.

The week ending June 5 closed with a sharp broad-based equity selloff, with the S&P 500 dropping approximately 2.65% on Friday alone to 7,383.73 from the prior session’s 7,584.32. Despite the single-session shock, the index still holds well above its rising 200-day moving average, and the weekly close did not break the bullish trend structure that has been in place since the early-year breakout. Beneath the headline drawdown, defensive sectors held up relatively better and long-duration Treasury bids picked up — a pattern consistent with this week’s Treasury Rotation flip to Risk-Off. Earnings season has wound down with broadly stable forward guidance, and macro data continues to trace a soft-landing path, but valuations, positioning, and concentration risk all argue for tactical respect of the framework’s defensive holdout.

At 7,383.73, the index sits +7.7% above its 200-day SMA of 6,858.26. That spread is comfortable enough to keep Signal 4 on the offensive 2x leveraged allocation, but it has tightened from the prior week as Friday’s selloff compressed the cushion. Volatility expanded on the week as expected, with the VIX moving off multi-month lows. The technical setup remains constructive in the aggregate — price above a rising 200-day, breadth still expanding versus a month ago — but the divergence between the trend signal and the Treasury Rotation signal is the kind of split that historically precedes either a pause in the trend or a stronger rotation into defense.

The Beta Rotation signal remains Risk-On with the XLU/SPY 4-week Rate of Change at -0.82%. Utilities continue to underperform the broad market over the trailing four weeks, with the negative RoC reflecting persistent flows out of defensive equity sectors. The persistence of this reading across multiple weeks supports the broader risk-on tilt and confirms that Friday’s selloff has not yet triggered a defensive sector rotation. The framework’s allocation stays on SPY.

The Treasury Rotation signal is Risk-Off on the May month-end reading. TLT returned 0.16% in May versus IEF at -0.35%, with the long bond outperforming the intermediate — a classic defensive risk-appetite signature. The signal will hold this May reading through the end of June. Long-duration outperformance during a backdrop of generally rising equity tells a story of yield-curve flattening pressure and creeping recessionary positioning at the long end. This is the lone defensive holdout in the framework this week and warrants close attention. A persistent Risk-Off Treasury signal alongside a Risk-On 200-day reading is the kind of divergence that historically signals an inflection point: either the equity trend resolves the divergence by following Treasuries lower, or Treasuries reconverge upward.

The Lumber/Gold signal is RISK-ON on the latest 13-week reading. Lumber’s 13-week return of 1.30% exceeds gold’s -11.72%. All seven Lumber/Gold sub-strategies are positioned offensively, with cyclical and growth-tilted pairs favored over defensive bond pairs. Lumber has held its bid as housing demand expectations firm, while gold has pulled back from its early-May highs and sold off sharply Friday alongside equities. The relative dynamic stays Risk-On and the spread actually widened on Friday’s gold decline — a re-acceleration in gold would be required to flip the signal.

The 3-1 Risk-On reading sits in the middle of the framework’s distribution. Mixed readings with one defensive holdout often precede broader pivots in either direction — either the holdout reconverges to the rest, or the rest converge to the holdout. The current setup demands tactical respect: maintain offensive allocations where signals call for them, but recognize that the Treasury Rotation flip and Friday’s broad equity selloff are coherent signals worth monitoring. The risks worth watching are an acceleration of the long-Treasury bid, a continued series of broad equity selloffs that compress the cushion above the 200-day, or a flip of the Lumber/Gold spread back to gold-favored.

SIGNAL 1: BETA ROTATION

Based on: “Opposing Behavioral Forces: Beta Rotation” (SSRN 2417974)

Target Investor: Self-directed investors who want to capture relative strength between equity market segments. This signal uses the 4-week rate of change of the Utilities-to-S&P 500 price ratio to determine whether the market favors offense (broad equity) or defense (Utilities).

CURRENT INDICATOR: RISK-ON

XLU/SPY 4-Week Rate of Change: -0.82%

Current Allocation: 100% SPY (S&P 500)

Growth of $100,000 | YTD from January 3, 2025 | Data: Lead-Lag Publishing, LLC

SIGNAL 2: TACTICAL RISK ROTATION

Based on: “A Quantitative Approach to Tactical Asset Allocation” (SSRN 2431022)

Target Investor: Conservative to moderate investors seeking a tactical overlay between equities and long-duration Treasuries. This signal compares the prior month total return of 10-year versus 30-year Treasury bonds to identify shifts in the yield curve’s risk appetite signal.

CURRENT INDICATOR: RISK-OFF

30yr Treasury (TLT) May Return: 0.16%

10yr Treasury (IEF) May Return: -0.35%

Current Allocation: 100% Long-Duration Treasuries (VLGSX/TLT)

Growth of $100,000 | Monthly Data from January 2025 | Data: Lead-Lag Publishing, LLC

SIGNAL 3: LUMBER/GOLD RATIO

Based on: “Lumber: Worth Its Weight in Gold” (SSRN 2604248)

Target Investor: Active investors seeking to rotate between offensive and defensive exposures across multiple asset class pairings. This signal uses the 13-week relative performance of Lumber futures versus Gold spot to determine the market’s risk appetite. When Lumber outperforms Gold, the economy is likely strengthening (Risk-On). When Gold outperforms, investors should favor defensive positioning (Risk-Off).

CURRENT INDICATOR: RISK-ON

Lumber 13-Week Return: 1.30%

Gold 13-Week Return: -11.72%

Lumber now outperforming Gold over 13 weeks. All 7 sub-strategies have rotated to offensive positioning.

Lumber/Gold Bond Rotation (SPY vs GOVT)

Growth of $100,000 | YTD from January 3, 2025 | Data: Lead-Lag Publishing, LLC

Lumber/Gold Buy-Write (SPY vs PBP)

Growth of $100,000 | YTD from January 3, 2025 | Data: Lead-Lag Publishing, LLC

Lumber/Gold Low Volatility (SPY vs SPLV)